If you’ve started thinking about your retirement, you may wonder how much you actually need to invest so you can live comfortably in retirement. With the cost of living crisis going on, finding that extra money to put away each month becomes harder and harder.

In this article, we’re going to take a look at whether or not £100 per month is enough to save for retirement. For some people it may be but for others it could be a long way off. Let’s take a look.

How Much £100 Per Month Is Worth At Retirement

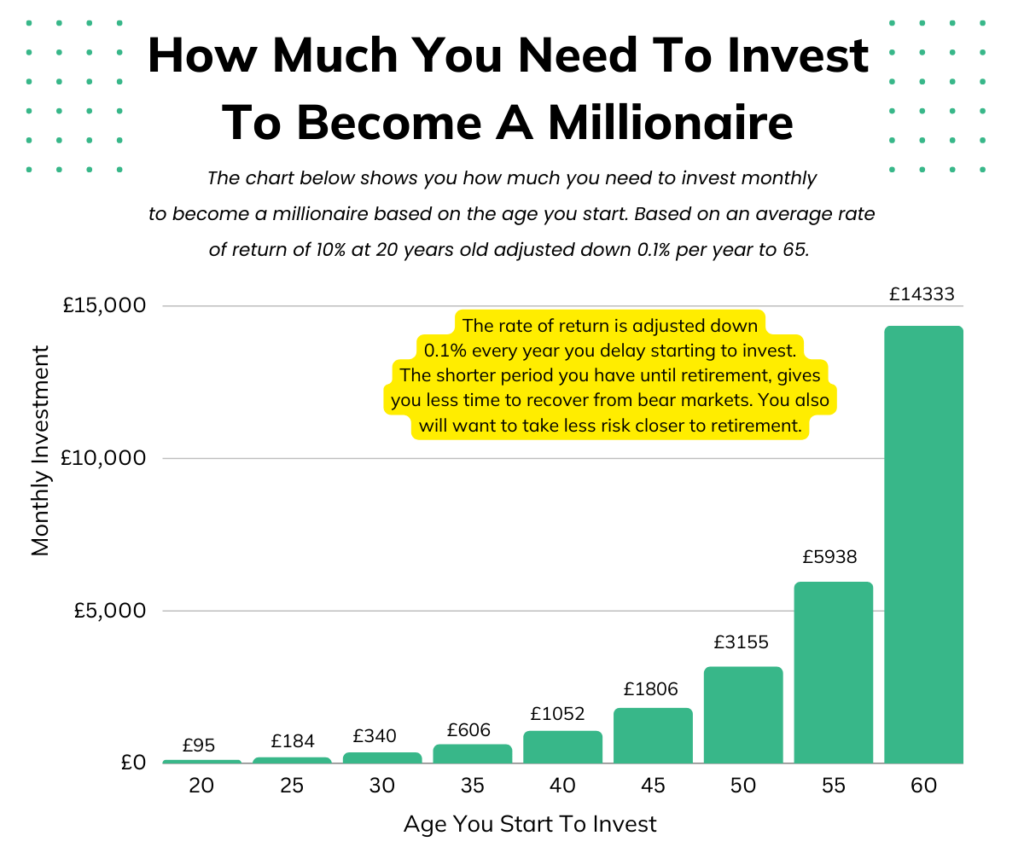

Most people start thinking seriously about retirement in their early 30s but that may be too late if you only want to contribute £100 per month. The table below shows how much you would have at retirement if you invested £100 per month at an average 10% return based on the age you start.

| Starting Age | Portfolio Value At 65 |

|---|---|

| 20 | £1,048,250 |

| 25 | £632,407 |

| 30 | £379,663 |

| 35 | £226,048 |

| 40 | £132,683 |

| 45 | £75,936 |

If you need £30,000 per year in retirement to live comfortably, you will need a portfolio of at least £750,000. When adjusting for inflation you will actually need more than that.

If you’re planning to only invest £100 per month, you need to be in your early 20’s if you want to reach a reasonable retirement portfolio before you turn 65.

If you are starting any later than that, you won’t be contributing enough to reach a sustainable retirement portfolio.

The chart below shows roughly how much you need to contribute to your portfolio depending on the age you are currently to reach £1 Million at retirement.

I would recommend using our FIRE Age calculator to see how much you need to invest to reach a portfolio value large enough to sustain your expected expenses.

How To Work Out How Much You Need To Invest To Reach Retirement

Below are some steps to take to work out how much you will need to invest on a monthly basis.

- Determine Your Retirement Goal: Before calculating how much to invest, you first need to decide the total amount you’d like to have by the time you retire. This will be based on your expected expenses, lifestyle, and any other sources of income (like the UK’s State Pension).

- Estimate the Number of Years Until Retirement: Decide at what age you’d like to retire and subtract your current age from it. This will give you the number of years you have to invest.

- Assume an Annual Rate of Return: This can be tricky as investment returns can vary. Historically, the stock market has returned about 7-9% annually after accounting for inflation. However, past performance doesn’t guarantee future results. To be conservative, you might assume a 7% annual return.

- Use a Compound Interest Calculator: With the information from steps 1-3, you can use a compound interest calculator to determine how much you need to invest each month. Input your current savings (if any), your expected rate of return, and the number of years you have left until retirement.

- Adjust for Inflation: The value of money tends to decrease over time due to inflation. In the UK, inflation rates have historically hovered around 2-3%. Remember to account for this in your calculations to ensure your retirement savings have the same purchasing power in the future.

- Consider Other Sources of Income: The UK has a State Pension, which can provide some income in retirement, depending on your National Insurance contribution history. Make sure to include this and any other pensions or income sources in your overall plan.

- Review Regularly: It’s essential to review your retirement plan and investment strategy periodically. As you approach retirement, your risk tolerance may change, and you might adjust your investments accordingly.

Let’s take a look at an example:

- Emma, 30 years old, wants to retire at 65 with £1 Million Invested

- She assumes a rate of return of 7% and has 35 years to invest

- Using a compound interest calculator, with £0 initial investment and aiming for £1 Million at retirement, she finds she needs to invest approximately £550 per month.

- If she accounts for inflation she may need to invest even more than that to reach a sustainable level of income.

Emma also has a state pension which will also pay here. Currently the state pension is £10,600 per year and may be higher when you retire.

Easy Method To Calculate Your Retirement Number

If you want to calculate a rough estimate you would need in retirement you can use this “back of the napkin formula to work it out”.

- Work out your expected annual expenses in retirement

- Subtract the state pension from your annual expenses

- Times that amount by 25 to get the portfolio value you need at retirement

- You can then use a compound interest calculator to work our how much you need to invest each month. I have included our compound interest calculator embedded below.

Want to retire earlier than 65? Check out this article on how much money you would need to never work again.

Where Should You Invest Your £100

Now you know how much you need to be investing each month, how do you actually get started? Let’s take a look.

Workplace Pension

If you are employed, the first thing you should be doing is maxing out your workplace pension up to the employer match. In the UK you must contribute 5% of your salary to your pension and your employer must contribute a minimum of 3%.

Your contributions are pre-tax lowering the amount of tax you will pay and your employer match is essentially free money. For most people it’s a good idea to contribute at least what your employer will match. This means you will maximise the amount of free money you are getting. It’s essentially 100% immediate returns. You won’t beat that elsewhere.

For example:

- You earn £30,000 and your employer will match up to 6% of your pension contributions. We have to remove the lower earnings threshold of £6,240 meaning your contributions will be based on qualifying earnings of £23,760.

- At 6% you would be contributing £118.80 per month from your pre-tax salary and your employer would be contributing another £118.80 on top of that giving you total monthly contributions of £237.60.

You are already way over the £100 mark we initially talked about. Even on a lower salary and lower employer contribution you would still hit £100 per month.

This is coming out before you even receive your salary so it’s a great way to invest without “feeling like your spending you money”.

Now the problem with this is your employer pensions usually have a default fund that is quite conservative. You may have access to change where your pension contributions are invested. This is worthwhile looking into.

Your pension contributions cannot be touched until the retirement age without penalty, so this strategy isn’t enough to “retire early”.

You may want to invest outside of your pension as well if you want to have funds you can access pre-officialy retirement. You can follow the steps below to start investing outside of a pension.

Investing Through An ISA

If you want to invest an extra £100 outside of your pension you can follow the steps below.

Brokerage

First you need to choose a brokerage. You can see our guide to the best brokerages for more details however for most people Trading 212 is a great option. It has access to a wide range of ETFs to invest in as well as zero commission trading. This allows you to invest with minimal fees.

Trading212 is a zero-commission trading platform offering general investment accounts, ISAs and CFD accounts. They are a trusted broker who has been around for almost 2 decades now. They have a range of features such as pies and multi-currency accounts which aren't offered by other brokerages.

- Commission Free Trading

- Access to over 12,000 Stocks and Funds

- Impressive features such as Pies and Multi-currency

- No phone support

Account Type

When you open you Trading 212 account, there is multiple options to choose from. You can open a general investment account or an ISA. Both act essentially the same however the ISA is a tax wrapper. It allows you to invest up to £20,000 per year and benefit from tax free gains.

Any gains you make in the appreciation of a stock are tax free as well as any dividends paid from stocks are tax free. This makes it an amazing option for building long term wealth.

Stocks & ETFs

Once your ISA is open you now have to decide where to invest your money. In my opinion, most people are best suited to a broad index fund. It allows you to be diversified by investing in the whole market and not relying on individual stocks. Index funds also have low fees which make them great for compounding returns over long periods of time.

Some of my favourite ETFs and Index funds are VUSA which is an S&P 500 index tracker and the Fidelity World Index which is a broad market Index fund investing all around the world.

You should do your own research to figure out what works best for you.

For more information on investing, check out our beginners guide to investing.

Final Thoughts

You should now know whether or not £100 is enough for you to invest for retirement. If you’re lucky enough to be reading this in your early 20s, £100 may well be enough to reach a £1 Million Portfolio. However, if you’re older, you should use the methods laid out above to calculate how much you actually need to invest to reach your retirement portfolio goal.

Read More From Moneysprout: